401(k) Early Withdrawal: How to Avoid the 10% Penalty

It is your money, but the IRS locks it behind a gate until you turn 59½. If you break the lock early, you pay a 10% penalty. But wait—if you know the secret codes (like the “Rule of 55”), you can unlock the gate early for free.

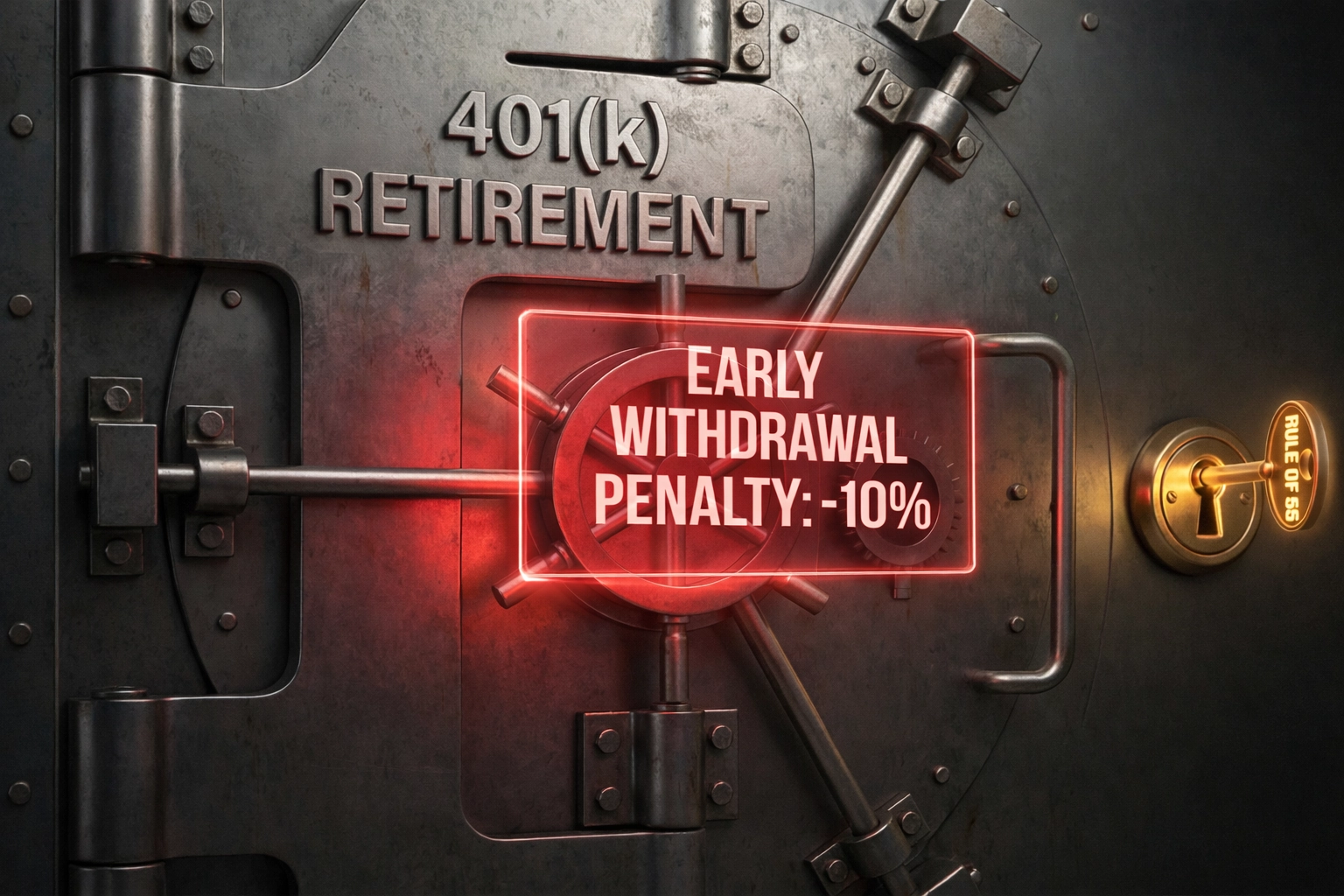

The Golden Key: Your 401(k) is a locked vault. Breaking in costs 10% (Penalty). But if you quit at 55, you get a special key to open it for free.

Image Source: bestmoneytip.com

The “Destruction of Wealth” Math

You think you are taking out $10,000. But after the IRS is done with you, it looks very different.

| Component | Cost (Est.) | You Keep |

|---|---|---|

| Withdrawal Amount | $10,000 | 100% |

| Federal Tax (22%) | -$2,200 | 78% |

| State Tax (~5%) | -$500 | 73% |

| Early Penalty | -$1,000 | 63% |

| Final Cash | $6,300 |

3 Ways to Escape the Penalty

1. The “Rule of 55” (Best for Early Retirees)

If you get fired, quit, or retire in the calendar year you turn 55 or older, you can withdraw from your current employer’s 401(k) without the 10% penalty.

Warning: This does NOT apply to old 401(k)s from previous jobs or IRAs. Only the account from the job you just left.

2. The SEPP / Rule 72(t) (Best for FIRE)

You can take money out at ANY age (even 35) penalty-free if you agree to take “Substantially Equal Periodic Payments” for at least 5 years or until age 59½.

Warning: You must stick to the strict schedule. If you stop or change the amount, the IRS will charge you all the past penalties plus interest.

3. Hardship Withdrawals (The “Emergency” Button)

The IRS allows penalty-free access for specific tragedies:

- Total Disability: If a doctor certifies you can never work again.

- Medical Debt: Unreimbursed medical expenses (>7.5% of AGI).

- Disaster Relief: Living in a FEMA-declared disaster zone (new SECURE 2.0 rule allows up to $22k).

- Domestic Abuse: Victims can withdraw up to $10k (or 50%) penalty-free.

Pro Tip: The “401(k) Loan” Hack

Don’t withdraw. Borrow.

Be Your Own Bank

The Pros: No taxes. No penalties. The interest you pay goes back into YOUR account, not to a bank.

The Risk: If you leave your job, you usually have to pay back the entire loan immediately, or it counts as a taxable withdrawal.