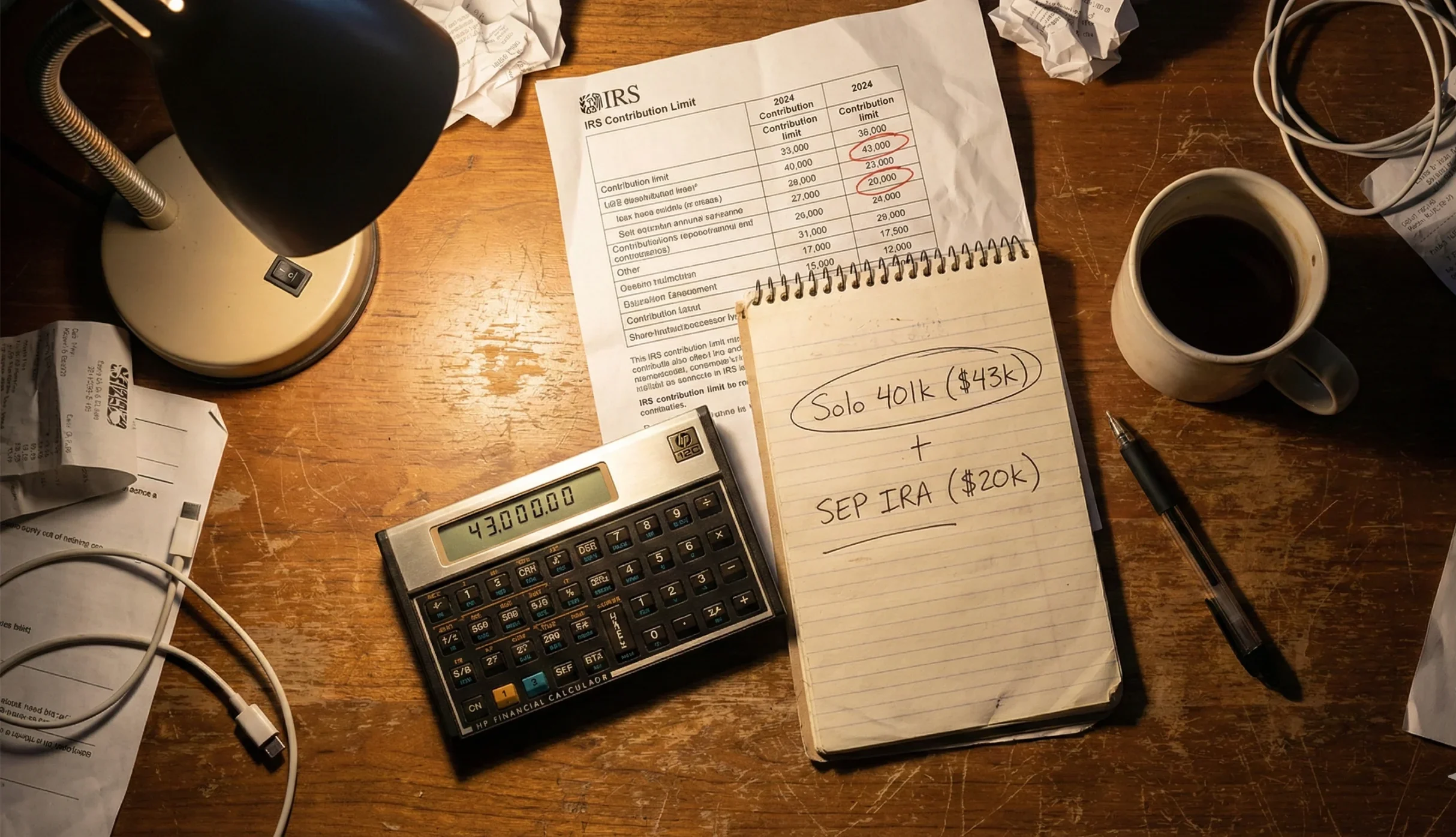

Solo 401k vs SEP IRA: Which Plan Builds Wealth Faster?

If you are self-employed, you have a superpower: you can choose your own retirement plan. The two heavyweights are the Solo 401k and the SEP IRA. Many CPAs recommend the SEP IRA because it is “easy.” But “easy” often costs you money. For most business owners earning under $200,000, the Solo 401k allows you to shelter significantly more cash from the IRS. Here is the math behind why the Solo 401k is usually the superior wealth-building machine.

The math rarely lies: One plan works harder for your money.

1. The Math: Why Solo 401k Wins on Limits

The SEP IRA has a fatal flaw: it only allows the “Employer” side of the contribution (approx. 20-25% of profit). The Solo 401k allows BOTH the Employee side ($23,000+) AND the Employer side.

2. Side-by-Side Showdown

It isn’t just about the limits. Flexibility matters.

| Feature | SEP IRA | Solo 401k |

|---|---|---|

| Contribution Limit | ~20-25% of Income | $23k + 20-25% of Income |

| Roth Option | No (Traditionally)* | Yes (Tax-Free Growth) |

| Loans | Not Allowed | Borrow up to $50k |

| Paperwork | Easy (Form 5305-SEP) | Medium (Form 5500-EZ > $250k) |

| Deadline | Tax Filing Date (Apr/Oct) | Must Open by Dec 31 |

*SECURE 2.0 Act introduced Roth SEP, but many custodians do not support it yet.

3. Strategy: The “Loan” Advantage

Liquidity is king. What if you need cash for your business?

- Borrow up to $50,000

- No Taxes or Penalties

- Interest paid to YOURSELF

- Cannot Borrow

- Must Withdraw (Taxable)

- 10% Penalty (if under 59.5)

4. Warning: The Employee Trap

“Solo” means Solo.

⛔ Do You Have Employees?

This is the one area where both plans can bite you.

- Solo 401k: If you hire a full-time employee (1000+ hours) who is NOT your spouse, you must terminate the Solo 401k and switch to a standard 401k (expensive).

- SEP IRA: If you contribute 20% of your salary to your SEP, you generally MUST contribute 20% of your eligible employee’s salary to their SEP. You cannot discriminate.