The 20/4/10 Rule Defined

To prevent financial overextension, follow the 20/4/10 rule when buying a car: Put down at least 20%, finance for no more than 4 years, and keep total monthly vehicle expenses (including insurance and gas) under 10% of your gross monthly income.

Most people buy cars based on what the bank approves, not what they can actually afford. This is a fatal financial mistake. The bank does not care about your retirement savings or your net worth; they only care if you can make the minimum payment. To build wealth, you need a strict guardrail. Enter the 20/4/10 Rule, the gold standard for vehicle affordability.

Before you debate New vs Used or Leasing vs Buying, you must first define your maximum mathematical budget.

Why the 20/4/10 Rule Exists

This isn’t an arbitrary restriction. Each number in the formula protects you from a specific financial risk:

- 20% Down Payment: Protects against the “Depreciation Gap.” Since cars lose ~20% of value in Year 1, putting 20% down ensures you are never “underwater” (owing more than the car is worth) immediately after driving off the lot.

- 4-Year Term (48 Months): Prevents interest drag. Extended loans (72 or 84 months) lower payments artificially but drastically increase total interest paid and keep you in debt while the asset rots.

- 10% of Income: Protects cash flow. Spending more than 10% of your gross income on transportation creates “Tax Drag” on your ability to invest in appreciating assets like stocks or real estate.

The Math: What You Can Actually Afford

Let’s apply this rule to different income levels. The results are often a wake-up call for buyers eyeing luxury vehicles.

| Annual Income | Monthly Budget (10%) | Max Car Price (Est.) |

|---|---|---|

| $50,000 | $416 / mo | $18,000 – $22,000 |

| $100,000 | $833 / mo | $35,000 – $40,000 |

| $150,000 | $1,250 / mo | $55,000 – $60,000 |

| $250,000 | $2,083 / mo | $90,000+ |

*Max price assumes 20% down and average insurance costs.

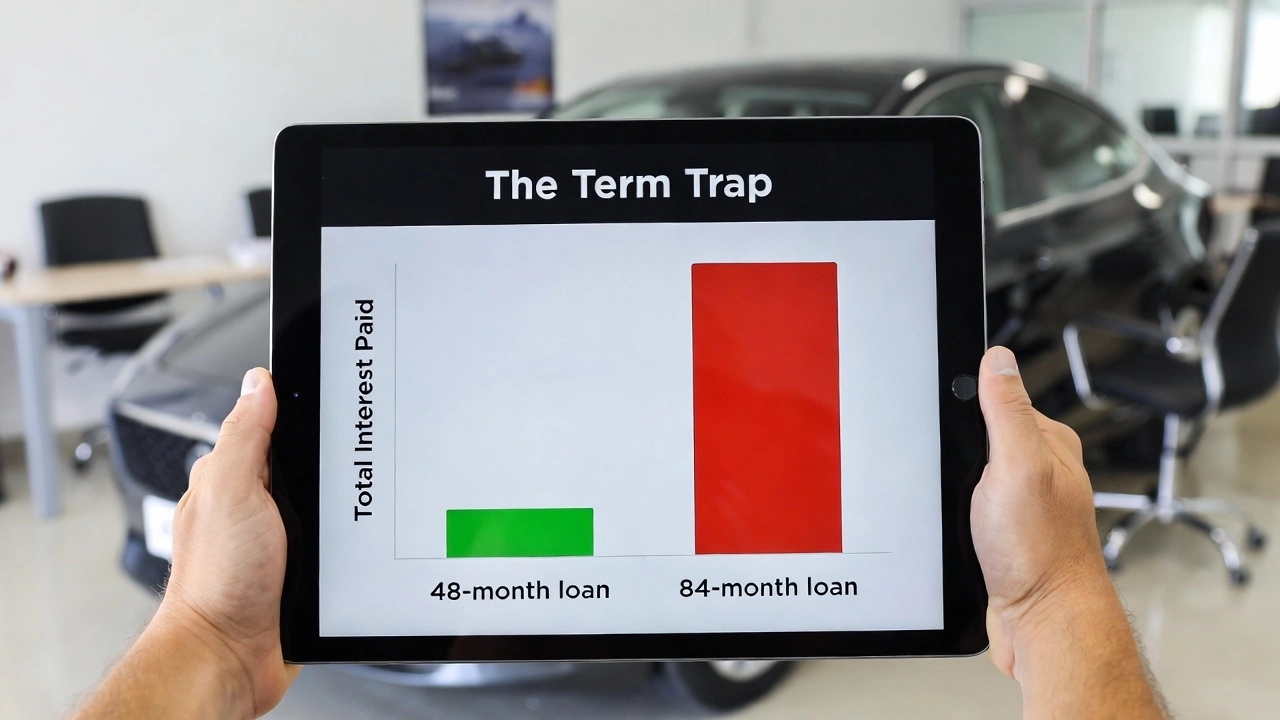

The “Term Trap”: 72 and 84-Month Loans

Dealerships love 84-month loans. Why? Because they allow them to sell you a $50,000 car on a $30,000 budget. Do not fall for this.

By extending the term to 84 months, you pay nearly double the interest ($10,800 vs $5,900). Worse, you will likely have negative equity for the first 5 years of the loan, trapping you in the vehicle.

When to Break the Rule

Rules are guidelines, not physics. There are exceptions where bending the 20/4/10 rule is acceptable:

The Safety Exception: If you are low-income but need a reliable car for work, buying a safe $10,000 vehicle with little money down is better than losing your job due to a breakdown.

The 0% APR Exception: If you have the cash to buy the car but the dealer offers 0% financing (rare), take the loan. Keep your cash in a high-yield account earning 4-5%.

Frequently Asked Questions

Does the 10% rule include insurance and gas?

Yes. Ideally, the “10%” limit covers the total cost of transportation: loan payment, insurance premiums, fuel/charging, and maintenance. If your loan payment alone is 10% of your income, you are likely “car poor” once insurance is added.

Is the 20/4/10 rule for gross or net income?

The strict version uses net income (take-home pay), but the standard definition uses gross income. Using net income is safer, but gross income is the industry standard for debt-to-income (DTI) calculations.

What if I can’t afford a car under this rule?

If the math doesn’t work, you have three options: save for a larger down payment (to lower the monthly hit), buy a cheaper used vehicle (see New vs Used Guide), or improve your credit score to secure a lower rate.

Should I pay cash for a car if I can?

Paying cash is always the lowest-risk option. However, if interest rates are low (< 4%) and your investments earn > 7%, financing can be mathematically optimal. In today’s high-interest environment (> 7%), cash is king.

Conclusion: Buy the Car You Can Afford, Not the Payment

The 20/4/10 rule is a filter. It filters out vehicles that will stifle your future financial growth. If a car doesn’t fit in this box, you cannot afford it yet. Drive what you can pay for today so you can drive whatever you want tomorrow.

Smart Spending Alert

Don’t walk into a dealership empty-handed. Financing is where dealers make their real profit. Before you shop, check our guide on Dealer Financing vs Credit Unions to get pre-approved and lock in a fair rate.