Property Tax Deduction Limits: Navigating State and Local Caps

Executive Summary

Paying annual property taxes is an inescapable reality of homeownership. While the IRS allows you to deduct these local tax payments from your federal taxable income, this deduction is strictly governed by the State and Local Tax (SALT) limit. For the 2026 tax year, recent legislation has significantly expanded this cap, allowing middle-class taxpayers to deduct a combined total of up to $40,400 in property and state income taxes.

For a mid-career professional reporting an income of $120,000, understanding the shifting SALT cap is critical. The $40,400 limit encompasses both your local property taxes and either your state income taxes or state sales taxes. [Tax Topic 503] Previously restricted to just $10,000, this newly expanded cap means that the vast majority of middle-class homeowners can now fully deduct their entire state and local tax burden without leaving any money on the table.

However, this expanded tax shield comes with new complexity. The IRS now enforces a phase-out for high earners: if your Modified Adjusted Gross Income (MAGI) exceeds $500,000, the allowable SALT deduction begins to incrementally decrease. [IRS Pub. 530] Furthermore, to claim any portion of your property taxes, your total itemized deductions must exceed the standard deduction threshold for your filing status, requiring careful year-end planning.

Structural Background

Before applying the newly expanded SALT cap, the IRS requires taxpayers to verify that the local taxes they paid actually qualify as deductible property taxes.

The “Ad Valorem” Requirement

To be deductible, a property tax must be an “ad valorem” tax, meaning it is assessed uniformly based entirely on the assessed value of the real estate. [IRS Pub. 530] It must also be levied for the general public welfare. If the tax is a flat fee per household rather than a percentage of the home’s value, it does not qualify for the federal deduction.

Excluding Local Assessments

Your annual county tax bill often includes itemized charges for local benefits that increase the value of your specific property, such as assessments for installing new sidewalks, water mains, or localized street lighting. Furthermore, itemized fees for specific services—like trash collection, water delivery, or Homeowners Association (HOA) dues—are explicitly non-deductible and must be subtracted from the total bill before reporting on Schedule A. [IRS Pub. 530]

Under the One Big Beautiful Bill, the restrictive $10,000 SALT cap was dramatically altered. The cap increased to $40,000 in 2025 and is designed to adjust upward by 1% annually, reaching $40,400 for the 2026 tax year. However, this relief is temporary; the cap is currently legislated to revert to the original $10,000 limit in 2030, making current-year deductions highly valuable. [IRS Pub. 530]

Risk Layer

Taxpayers frequently make reporting errors regarding when and how their property taxes were actually paid, leading to disallowed deductions during an IRS review.

The Escrow Account Trap

If you have a mortgage, your monthly payment likely includes a portion dedicated to an escrow account, which your lender manages to pay your property taxes on your behalf. A common audit trigger occurs when homeowners deduct the total amount they paid into the escrow account during the year. The IRS strictly prohibits this. You may only deduct the exact amount that the lender actually transferred out of the escrow account and paid to the local tax authority during the calendar year. [IRS Pub. 530] This verified amount is reported to you on Form 1098.

Taxes Paid at Closing

When you buy or sell a home, the real estate taxes for that year are prorated between the buyer and the seller based on the number of days each party owned the property. You can only deduct the taxes allocated to the specific days you owned the home. [Tax Topic 503] If you pay the seller’s portion of the taxes at closing without being reimbursed, you cannot deduct that amount; instead, it must be added to the cost basis of the home.

Strategic Framework

For a DIY investor owning a $500,000 home, determining the actual value of the property tax deduction requires coordinating it with your state income tax burden against the new 2026 limits.

Actionable SALT Calculation Steps

To accurately report your deductible property taxes and maximize your benefit, follow this step-by-step procedure before finalizing your Schedule A:

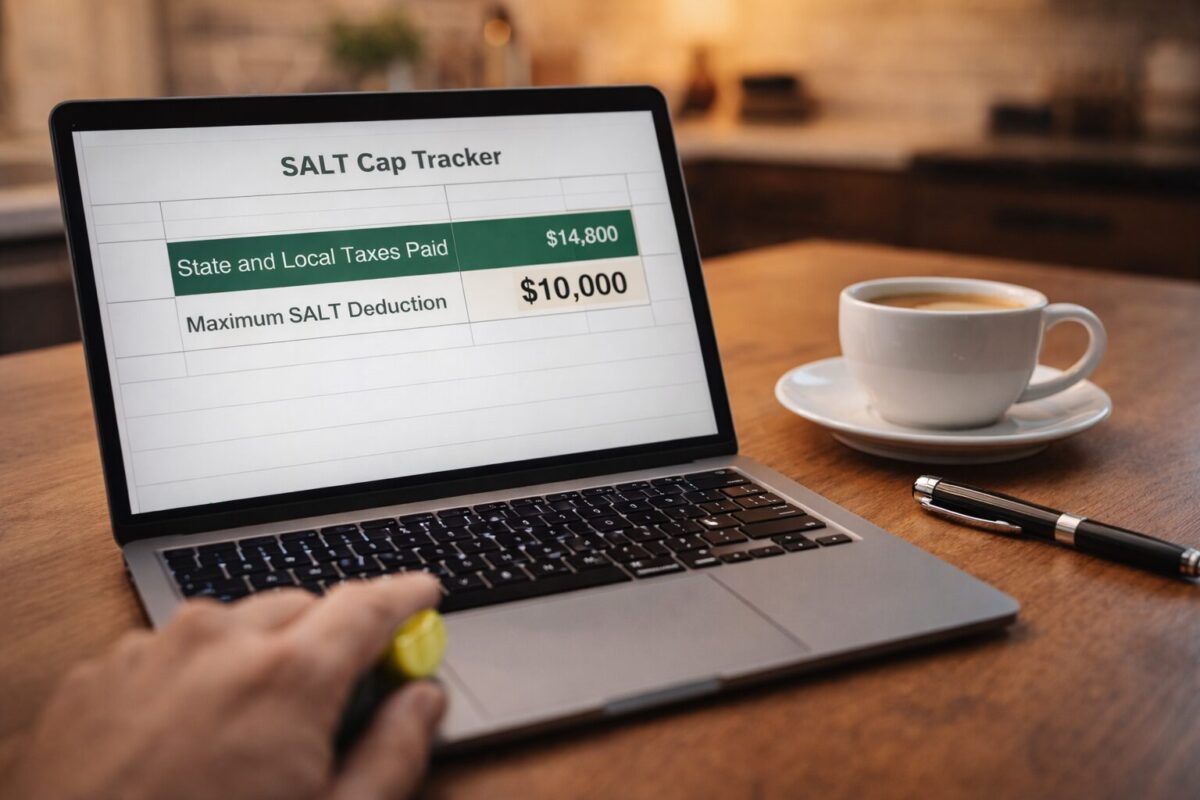

- Determine State Income Tax: Calculate your total state income taxes withheld from your W-2s and any estimated quarterly payments made during the year. Assume this total is $8,000.

- Audit Your Property Tax Bill: Obtain your official county tax bill. Identify the total amount paid (e.g., $9,500). Subtract any non-deductible fixed fees for trash collection or special local assessments. Assume the qualifying ad valorem tax is exactly $9,000.

- Combine and Verify Limits: Add your state income tax ($8,000) and your qualifying property tax ($9,000) for a total of $17,000. Under the old rules, you would lose $7,000 of this deduction. However, for 2026, because the new cap is $40,400 (and assuming your MAGI is under $500,000), your entire $17,000 is fully deductible. [Tax Topic 503]

- Evaluate Total Deductions: Add your fully deductible $17,000 SALT amount to your mortgage interest and charitable contributions. If the combined total exceeds your standard deduction, file Schedule A to secure the lower taxable income.

| Taxpayer Scenario (Middle-Class) | Old Rules (Pre-2025) | New 2026 Rules (One Big Beautiful Bill) |

|---|---|---|

| State Income Tax Paid | $8,000 | $8,000 |

| Property Tax Paid | $9,000 | $9,000 |

| Combined Total SALT | $17,000 | $17,000 |

| Allowed Fed Deduction | Capped at $10,000 (Lost $7k) | Fully Deductible $17,000 (Under $40.4k cap) |

If you own investment real estate, property taxes paid on those rental properties are claimed on Schedule E (Supplemental Income and Loss). Rental property taxes are treated as business expenses and are completely exempt from the personal SALT cap restrictions. [IRS Pub. 527]

Frequently Asked Questions

Yes. You can deduct property taxes paid on multiple personal residences, including a second home or vacation cabin. However, the combined total of all property taxes and state income taxes across all personal properties is still strictly subject to the $40,400 overall SALT limit for 2026. [IRS Pub. 530]

No. Under current tax statutes, individuals are prohibited from deducting foreign taxes paid on real estate as an itemized deduction on Schedule A. Only domestic property taxes qualify for the SALT deduction. [IRS Pub. 530]

You can only deduct the actual ad valorem tax amount. Any fines, late fees, or interest charges imposed by the local government for delinquent property tax payments are explicitly non-deductible for federal tax purposes. [Tax Topic 503]

If you itemized your deductions and claimed a tax benefit for paying the property tax in one year, and you receive a refund for those taxes in a subsequent year, you generally must include the refunded amount in your taxable income for the year you receive it, up to the amount of the tax benefit you originally received. [IRS Pub. 525]

Series

Real Estate Tax Strategies Guide

2 of 9 articles published

Data Sources & References

- [1] Internal Revenue Service (IRS) — Publication 530: Tax Information for Homeowners

- [2] Internal Revenue Service (IRS) — Tax Topic 503: Deductible Taxes