Mortgage Interest Deduction Limits: Navigating the $750k IRS Cap

Executive Summary

For homeowners, the mortgage interest deduction has historically been one of the most valuable tax benefits available. However, under current tax law, you cannot automatically deduct all the interest you pay. The IRS strictly limits this deduction to the interest paid on the first $750,000 of your qualifying mortgage debt. [IRS Pub. 936]

If you purchased a home recently and took out an $850,000 mortgage, the interest paid on the final $100,000 of that loan is considered non-deductible personal interest. The $750,000 cap ($375,000 if married filing separately) applies to mortgages originated after December 15, 2017. [IRS Pub. 936] This provision requires taxpayers in high-cost real estate markets to manually calculate their deductible percentage rather than simply relying on the year-end Form 1098 provided by their lender.

Because the mortgage interest deduction is an itemized deduction, it is only financially beneficial if your total itemized expenses—including your mortgage interest, charitable donations, and capped state taxes—exceed the IRS standard deduction for your filing status. Understanding how this $750,000 cap interacts with your other financial obligations is critical for projecting your tax liability and making informed decisions about paying down principal versus investing excess cash.

Structural Background

To accurately claim your mortgage interest on Schedule A, you must classify your debt based on when the loan was established and how the funds were utilized.

The Grandfather Clause

The IRS applies different limits based on your loan origination date. If you finalized your mortgage on or before December 15, 2017, your debt is grandfathered under the previous rules. For these older loans, you are permitted to deduct interest on up to $1,000,000 of qualifying debt. [IRS Pub. 936] If you refinance a grandfathered loan, the new loan retains the $1,000,000 limit, but only up to the remaining principal balance of the old loan at the time of refinancing.

Qualifying Residences

The $750,000 limit is a combined total that applies to your primary residence and one designated second home (such as a vacation cabin). You cannot deduct interest on the first $750,000 of your primary home and another $750,000 on a second home; the absolute ceiling for all qualifying residential debt combined is $750,000 per tax return. [IRS Pub. 936]

The $750,000 limit was introduced by the Tax Cuts and Jobs Act (TCJA) and is scheduled to expire at the end of 2025. Unless Congress passes new legislation, the deduction limit will revert to the original $1,000,000 threshold for the 2026 tax year, regardless of when the home was purchased.

Risk Layer

Many homeowners inadvertently violate IRS rules when taking out secondary loans against their home’s equity, leading to disallowed deductions during audits.

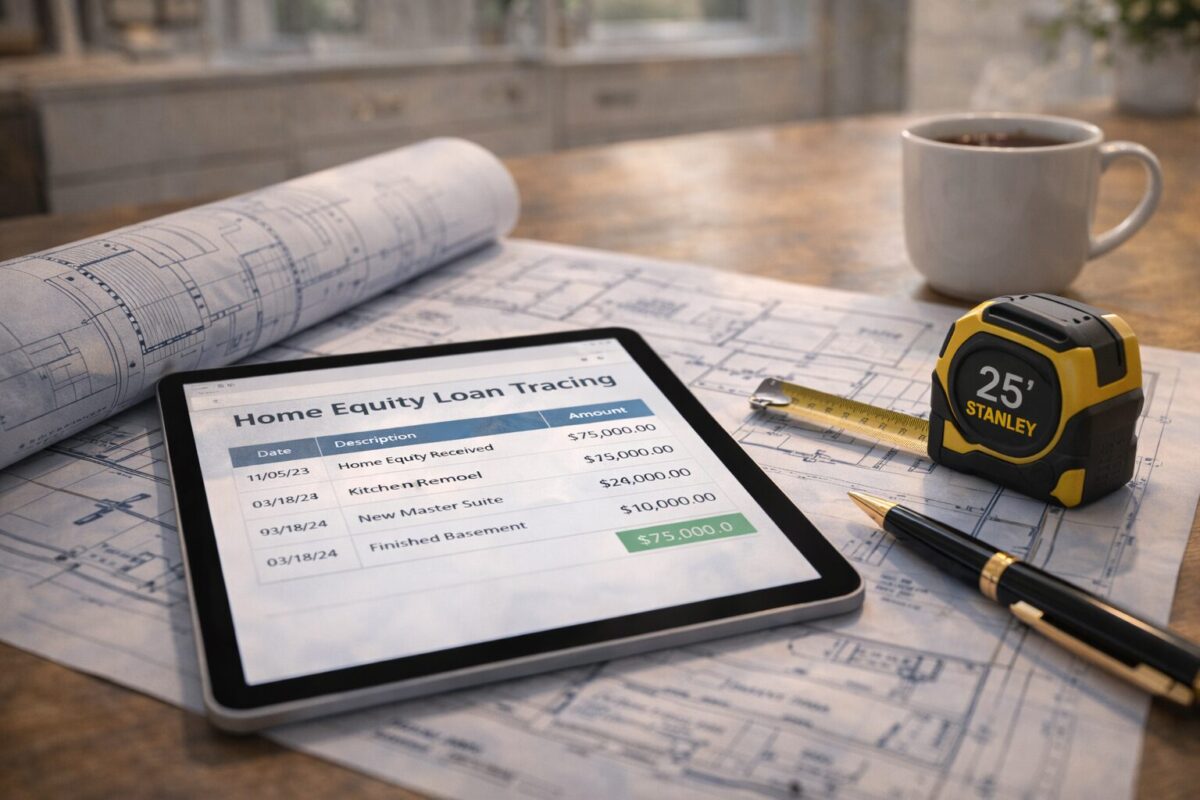

The HELOC “Personal Use” Trap

Home Equity Lines of Credit (HELOCs) and home equity loans are heavily scrutinized by the IRS. Interest paid on a HELOC is only deductible if the borrowed funds are strictly used to “buy, build, or substantially improve” the specific home that secures the loan. [IRS Pub. 936]

If you take out a $50,000 HELOC and use the funds to pay off high-interest credit cards, fund a child’s college tuition, or purchase a vehicle, the interest on that $50,000 is considered non-deductible personal interest. You must maintain clear financial tracing. If you use a HELOC for a mix of home renovations and personal expenses, you are required to allocate the interest and only deduct the portion directly tied to the home improvement.

Strategic Framework

If your mortgage exceeds the IRS limits, your year-end Form 1098 from the bank will display more interest than you are legally allowed to deduct. You must manually calculate your allowable deduction before filing.

Actionable Calculation Steps

Assume you purchased a home in 2023 with an $900,000 mortgage. Over the course of the year, you paid $54,000 in interest. To determine your deductible portion, follow this procedure:

- Determine Average Balance: Check your mortgage statements to confirm your average principal balance for the year. (For this example, we will use the $900,000 starting balance).

- Calculate the Deductible Percentage: Divide the IRS limit ($750,000) by your actual loan balance ($900,000). The result is 0.833, or 83.3%. [IRS Pub. 936]

- Apply to Total Interest: Multiply your total interest paid ($54,000) by the deductible percentage (83.3%). Your allowable Schedule A deduction is $44,982. The remaining $9,018 is non-deductible.

- Evaluate Total Itemized Deductions: Add this $44,982 to your capped State and Local Taxes ($10,000) and charitable contributions to confirm it exceeds your standard deduction.

| Loan Characteristic | Grandfathered Loan (Pre-Dec 15, 2017) | Current Law Loan (Post-Dec 15, 2017) |

|---|---|---|

| Acquisition Debt Limit | $1,000,000 maximum principal balance. | $750,000 maximum principal balance. |

| Refinancing Rules | Retains $1M limit up to the old balance. | Subject to the $750k limit. |

| HELOC for Remodeling | Deductible (up to combined limit). | Deductible (up to combined $750k limit). |

| HELOC for Personal Use | Not deductible under current TCJA rules. | Not deductible. |

For DIY investors holding significant cash, running this specific calculation is vital. If your loan balance is well above $750,000, paying down the principal that sits above the IRS cap guarantees an immediate, risk-free return by eliminating non-deductible interest from your household budget.

Frequently Asked Questions

Yes, discount points (prepaid interest) are generally deductible in the year you pay them, provided the loan is used to buy or build your primary residence and the points are computed as a percentage of the loan amount. Points paid for refinancing must usually be amortized over the life of the new loan. [IRS Pub. 936]

The $750,000 limit only applies to personal-use properties (Schedule A). If you hold a mortgage on a rental property, the interest paid on that specific loan is considered a business expense and is fully deductible on Schedule E, completely separate from the personal $750,000 limit. [IRS Pub. 527]

No. HOA fees, homeowners insurance premiums, and principal payments are strictly prohibited from being deducted on your tax return. Only the interest portion of your loan payment and qualifying property taxes are eligible for federal deductions. [IRS Pub. 530]

If you are married but choose to file your taxes separately, the mortgage interest deduction limit is cut in half. For loans originated after December 15, 2017, the limit is $375,000 per spouse. [IRS Pub. 936]

Series

Advanced Tax Deductions & Audit Defense

8 of 9 articles published

Data Sources & References

- [1] Internal Revenue Service (IRS) — Publication 936: Home Mortgage Interest Deduction

- [2] Internal Revenue Service (IRS) — Publication 530: Tax Information for Homeowners