Got a 1099-C? How to Avoid Paying Taxes on Forgiven Debt

You finally settled your credit card debt or negotiated a short sale on your home. You feel free. Then, in January, a form arrives in the mail: Form 1099-C (Cancellation of Debt). The IRS considers forgiven debt as “Taxable Income.” Suddenly, you owe the government money on money you never saw. Before you panic, check if you qualify for the Insolvency Exception—the CPA’s secret weapon to wipe out this tax bill.

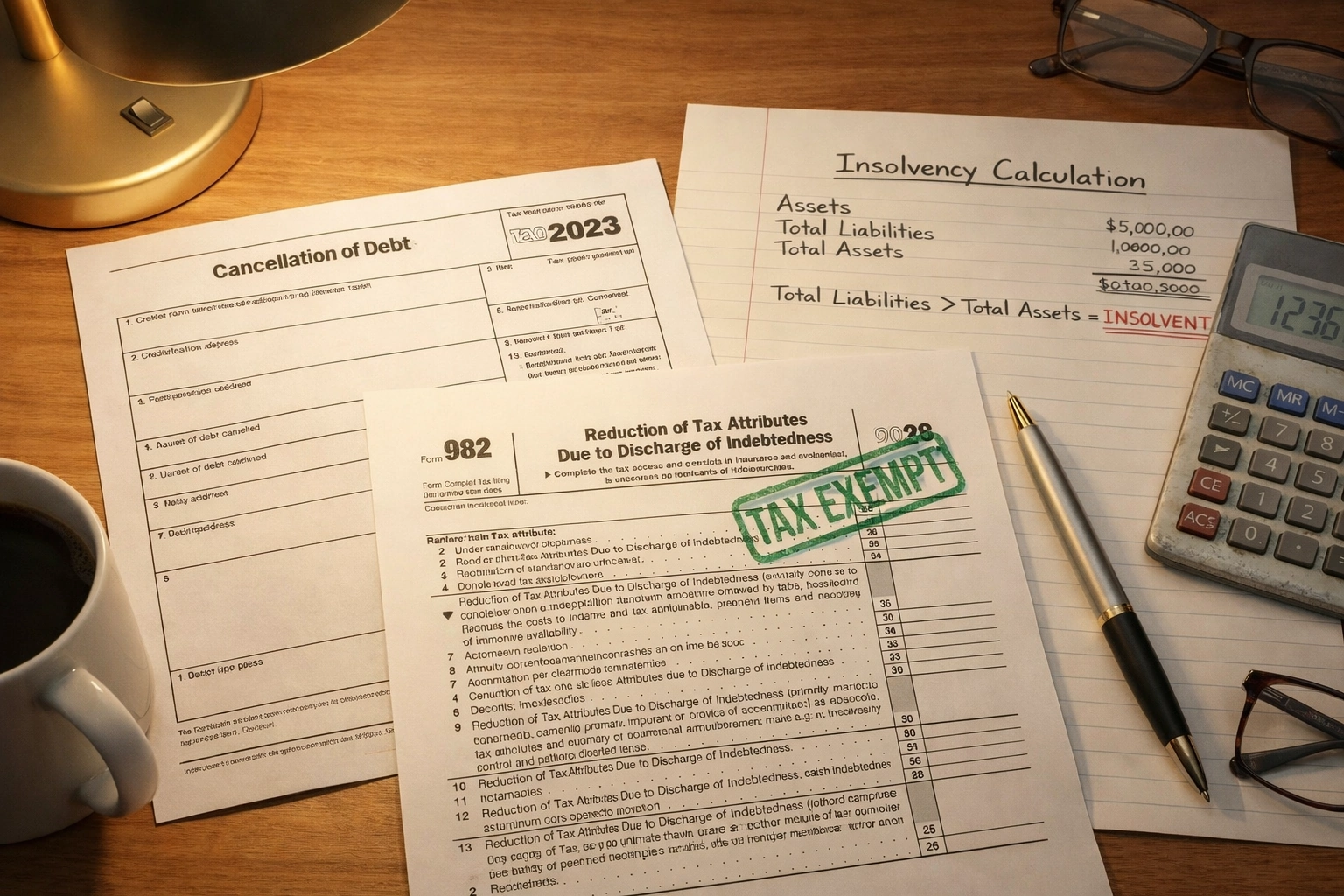

The Paperwork Shield: The 1099-C says you owe tax. The Insolvency Worksheet proves you were broke. Form 982 tells the IRS, “I’m exempt.” This trio saves you thousands.

Image Source: bestmoneytip.com

1. Why Is Forgiven Debt Taxable?

To the IRS, borrowing money is not income because you have to pay it back. But the moment you don’t have to pay it back, that money becomes a financial benefit—essentially, income.

- You owed: $20,000

- You settled for: $10,000

- Forgiven Amount: $10,000

- IRS sees: You “earned” $10,000.

- Tax Bill: At a 22% bracket, you owe $2,200 in taxes.

2. The “Insolvency” Escape Hatch

You do not pay tax on forgiven debt to the extent that you were insolvent immediately before the cancellation.

Self-Test Worksheet

| Category | Example Items | Your Value (Estimate) |

|---|---|---|

| A. Total Liabilities (What you owe) |

Mortgage, Car Loans, Student Loans, Credit Cards, Medical Bills (Everything). | $150,000 |

| B. Total Assets (What you own) |

Home Value, Car Value, 401(k), Bank Accounts, Furniture. | -$130,000 |

| C. Insolvency Amount (A minus B) |

How much you are “underwater.” | $20,000 |

The Verdict

3. How to File: Form 982

This does not happen automatically. If you ignore the 1099-C, the IRS computer will send you a bill. You must tell them, “I was insolvent.”

- Step 1: Download IRS Form 982.

- Step 2: Check Box 1b (“Discharge of indebtedness to the extent insolvent”).

- Step 3: Enter the amount of debt forgiven in Line 2.

- Step 4: Attach it to your Form 1040 tax return.

- Step 5: Keep your “Insolvency Worksheet” (from Section 2) in your records in case of an audit.

4. Other Ways to Avoid the Tax

Not insolvent? You might still qualify for other exclusions.