Capital Loss Carryover: How to Turn Bad Trades into Tax Breaks

Did you take a hit in the market? The IRS offers a path to recovery. You can use realized losses to lower your taxable income—not just this year, but potentially for decades. Here is how the $3,000 deduction limit and Carryover Rule work as of 2026.

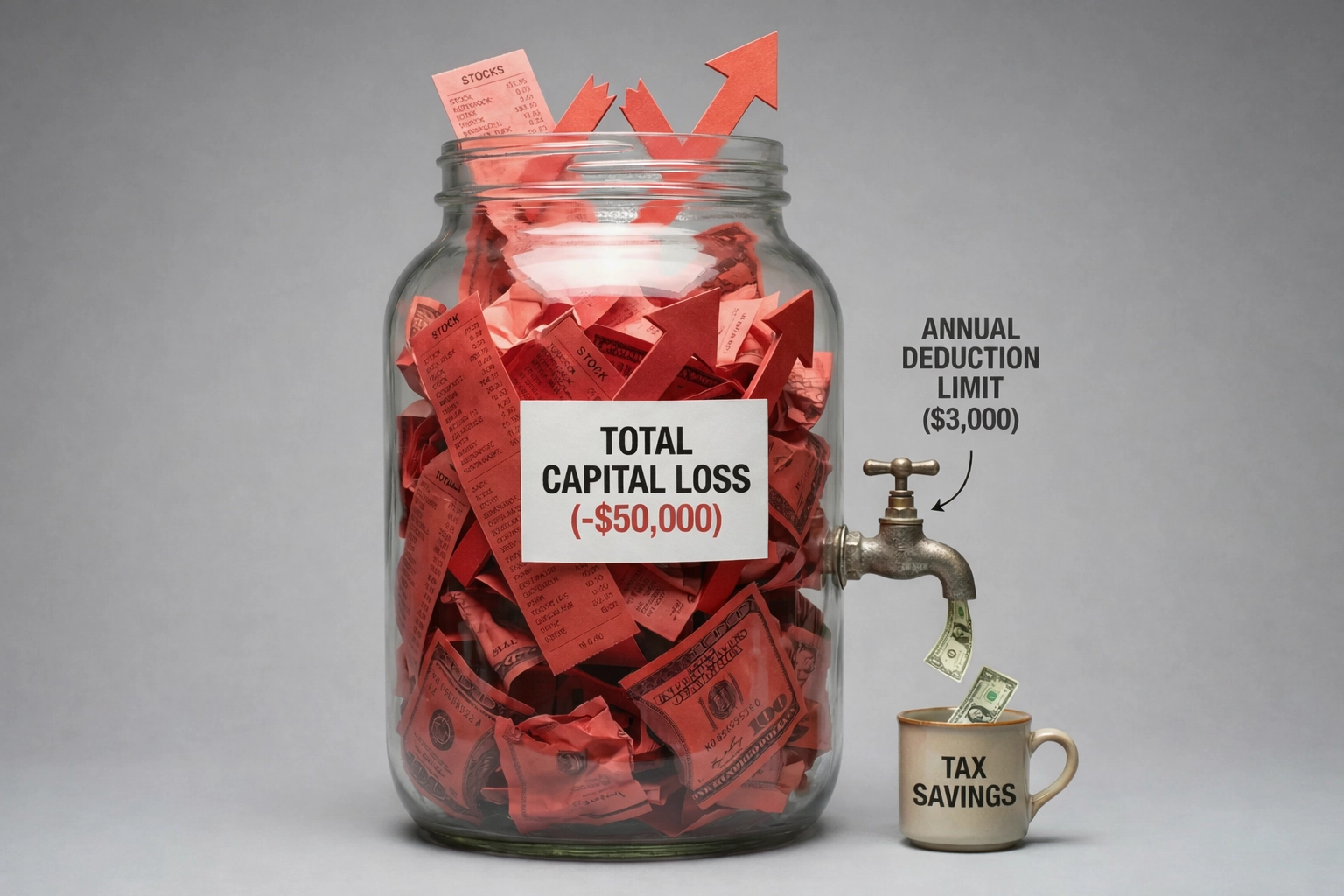

The $3,000 Drip: You may have a massive tank of losses (Red), but the IRS only gives you a tiny spigot. You can only fill the “Tax Savings” cup $3,000 at a time per year.

Image Source: bestmoneytip.com

1. The $3,000 “Faucet” Rule

Think of a large capital loss as a water tank. The IRS allows you to open the tap only slightly ($3,000) each year to lower your wage taxes.

| Scenario | Your Stock Result | Tax Impact (2026) |

|---|---|---|

| Scenario A | +$10,000 Profit | Pay Cap Gains Tax |

| Scenario B | -$2,000 Loss | Deduct $2,000 (Full) |

| Scenario C | -$50,000 Loss | Deduct $3,000 (Max) |

What happens to the remaining $47k?

2. Visualizing the “Carryover” Flow

Let’s say you realized a $20,000 loss in Year 1. You don’t lose that tax benefit; you just use it slowly over time.

| Year | Starting Loss | Deduction Used | Remaining Balance |

|---|---|---|---|

| Year 1 | -$20,000 | -$3,000 | |

| Year 2 | -$17,000 | -$3,000 | |

| Year 3 | -$14,000 | -$3,000 | |

| Year 4+ | … | -$3,000/yr |

3. Pro Strategy: Tax Loss Harvesting

Don’t just wait for losses to happen. Strategic investors create losses intentionally to offset gains. This is called Tax Loss Harvesting.

Step 1: Sell Stock A and realize the $4,000 loss.

Step 2: Immediately buy a competitor (Stock B) or a Sector ETF.

Result: You maintain market exposure while banking a $4,000 tax deduction to offset other gains or wages.

Why swap stocks?

4. Warning: The “Wash Sale” Rule

The IRS prevents taxpayers from claiming artificial losses. The 30-Day Rule is the primary enforcement mechanism.

The 30-Day Scenario

- Dec 1: You sell 100 shares of Tesla at a $5,000 loss.

- Dec 15: You panic and buy back 100 shares of Tesla.

- Result: Since the purchase was within 30 days, the $5,000 loss is disallowed.

The disallowed loss is not vanished; it is added to the cost basis of the new shares. Essentially, your tax benefit is deferred until you sell the new shares.