Rental Property Tax Deductions: A Guide for Real Estate Investors

Executive Summary

When you own and operate a rental property, the rental income you receive from tenants is fully taxable. However, the IRS allows you to deduct the ordinary and necessary expenses incurred to manage, conserve, and maintain the property. By systematically tracking these expenses on Schedule E (Form 1040), real estate investors can significantly reduce their taxable rental income, sometimes shielding the cash flow entirely.

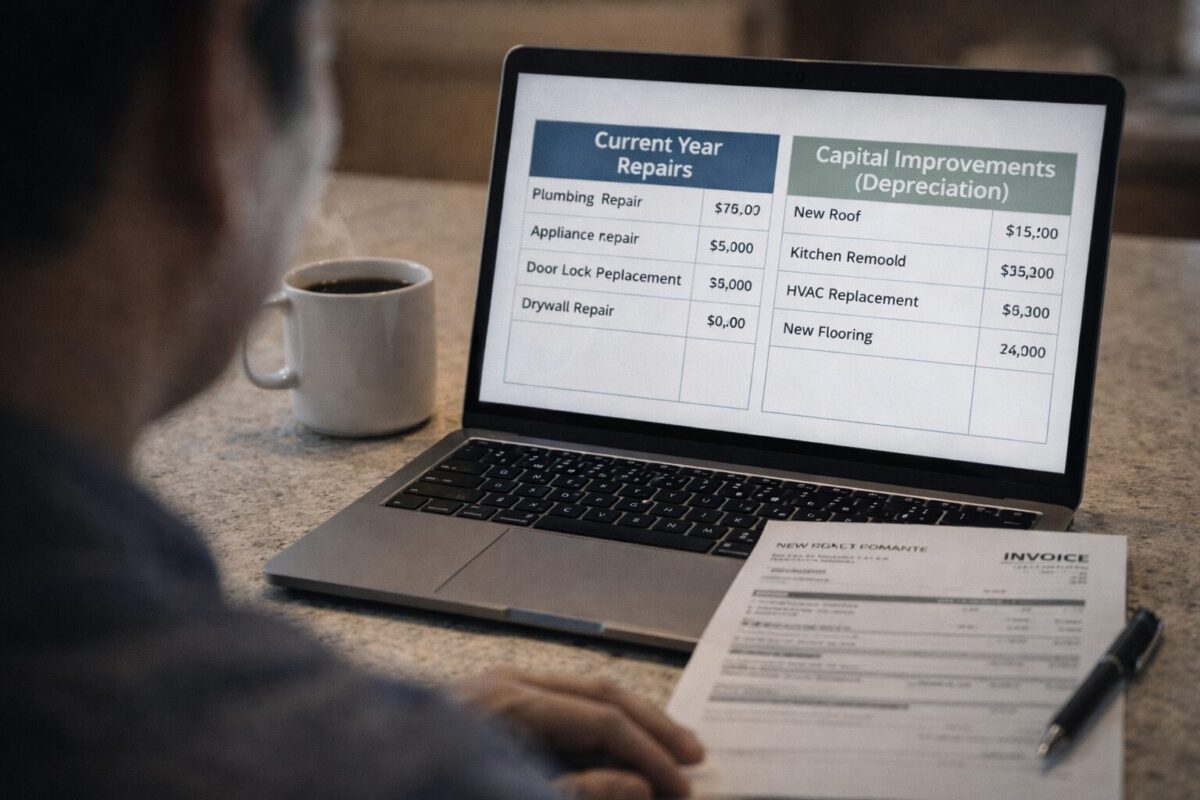

For a DIY investor managing a $400,000 rental home, understanding which expenses can be deducted immediately in the current year and which must be spread out over decades is the cornerstone of real estate tax strategy. Current-year deductions include property management fees, mortgage interest, insurance premiums, and routine maintenance. [IRS Pub. 527] These operational costs are directly subtracted from your gross rental income.

In contrast, major upgrades that add value to the property—such as a new roof or a kitchen remodel—cannot be deducted all at once. They must be capitalized and depreciated over 27.5 years. [IRS Pub. 527] Misclassifying an improvement as a routine repair is one of the most common triggers for an IRS audit. Proper documentation and a clear understanding of the tax code are essential to legally optimize your rental property’s financial performance.

Structural Background

To accurately file your taxes, you must understand the IRS framework separating operational expenses from long-term capital investments.

Repairs vs. Improvements

A “repair” keeps your property in good, working condition without adding significant value or prolonging its useful life (e.g., fixing a leaky pipe, painting a bedroom, replacing a broken window). These are fully deductible in the year they are paid. An “improvement” adds value, adapts the property to new uses, or prolongs its life (e.g., installing central air conditioning, building a deck). Improvements must be depreciated. [IRS Pub. 527]

The Depreciation Deduction

Depreciation is arguably the most powerful deduction for real estate investors. The IRS assumes that physical buildings degrade over time. You are allowed to deduct the cost basis of the residential building (excluding the land value) over a 27.5-year period. [IRS Pub. 527] This creates a “paper loss” that reduces your taxable income without requiring you to spend actual cash in the current year.

You can deduct the standard mileage rate for driving to your rental property to collect rent, perform maintenance, or manage the premises. However, if you travel strictly for the purpose of improving the property, those travel costs must be capitalized and added to the property’s basis rather than deducted immediately. [IRS Pub. 527]

Risk Layer

Many new landlords assume that if their rental property generates a net loss on paper, they can use that loss to offset their primary W-2 salary. This assumption often leads to severe compliance errors.

The Passive Activity Loss (PAL) Limit

The IRS categorizes standard rental real estate activities as “passive” income. As a general rule, you cannot use passive losses to offset active income (like your W-2 salary or active business income). [IRS Pub. 925] If your rental deductions exceed your rental income, the resulting loss is typically suspended and carried forward to future tax years until you either generate passive income or sell the property.

The $25,000 Special Allowance Phase-Out

There is a limited exception: if you “actively participate” in managing the rental, you can deduct up to $25,000 of rental losses against your active W-2 income. However, this allowance phases out quickly for high earners. If your Modified Adjusted Gross Income (MAGI) is between $100,000 and $150,000, the $25,000 allowance is incrementally reduced. If your MAGI is above $150,000, the allowance is entirely eliminated. [IRS Pub. 925] Only those who qualify for Real Estate Professional Tax Status can bypass these passive loss limitations completely.

Strategic Framework

To maximize your current-year deductions and ensure compliance, you must establish strict bookkeeping procedures specifically tailored for Schedule E.

Actionable Deduction Checklist

Implement the following procedures to systematically capture all allowable rental deductions:

- Isolate Property Taxes and Mortgage Interest: Unlike your primary residence, the interest and taxes paid on an investment property are not restricted by the personal $750k mortgage limit or the $10,000 SALT cap. Ensure you report these entirely on Schedule E, not Schedule A.

- Apportion the Land Value: When setting up your depreciation schedule, obtain your county property tax assessment to determine the ratio of land value to building value. You can only depreciate the building. (e.g., If you bought a property for $400,000 and the county assesses the land at 20%, your depreciable basis is $320,000).

- Utilize the De Minimis Safe Harbor: The IRS allows taxpayers to make an annual election to immediately deduct any tangible property expense (like an appliance or a minor renovation) that costs $2,500 or less per invoice. [IRS Pub. 535] Ensure your CPA attaches this specific election statement to your return.

- Track Prorated Expenses: If you rented out a single room in your home, or if you lived in a multi-family duplex while renting out the other units, you must strictly prorate expenses (like utilities and internet) based on square footage.

| Expense Type | Classification | Tax Treatment |

|---|---|---|

| Fixing a broken toilet | Routine Repair | 100% Deductible in Current Year |

| Replacing the entire roof | Capital Improvement | Depreciated over 27.5 Years |

| Property Management Fees | Operational Expense | 100% Deductible in Current Year |

| Buying a $1,500 Refrigerator | Equipment (Safe Harbor) | Deductible if De Minimis Election is filed |

By capturing every operational expense and utilizing depreciation, many investors generate a tax-free cash flow in the early years of ownership. However, remember that claimed depreciation will eventually be subject to taxes when you sell, unless you utilize a 1031 Exchange to defer the capital gains.

Frequently Asked Questions

No. The IRS strictly prohibits landlords from deducting the monetary value of their own time or physical labor spent repairing or maintaining the property. You may only deduct the actual cost of the tools and materials you purchased for the project. [IRS Pub. 527]

Yes. If the rental property is subject to HOA dues or condominium assessments, those fees are considered an ordinary and necessary operational expense and are fully deductible on Schedule E. [IRS Pub. 527]

Under the “Augusta Rule,” if you rent out your personal residence for fewer than 15 days during the calendar year, the IRS does not require you to report the rental income. However, because the income is tax-free, you are also strictly prohibited from deducting any rental expenses related to those days. [IRS Pub. 527]

Generally, no. Travel expenses incurred while searching for a new property, investigating its viability, or attending real estate investment seminars are considered non-deductible personal expenses or start-up costs, not current-year operational expenses for your existing Schedule E properties. [IRS Pub. 527]

Series

Real Estate Tax Strategies Guide

6 of 9 articles published

Data Sources & References

- [1] Internal Revenue Service (IRS) — Publication 527: Residential Rental Property

- [2] Internal Revenue Service (IRS) — Publication 925: Passive Activity and At-Risk Rules