Section 121 Exclusion Guide: Rules for Selling Your Primary Residence

Executive Summary

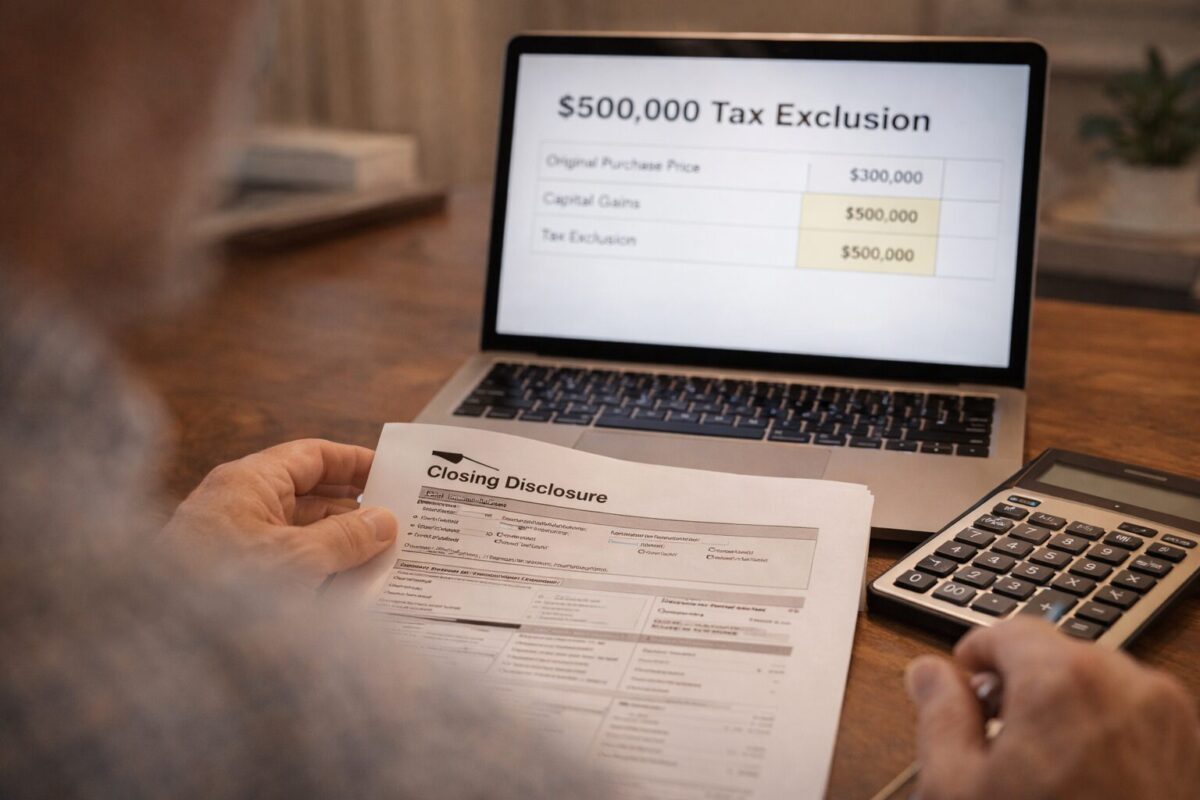

Internal Revenue Code Section 121 is a tax provision that allows qualifying homeowners to exclude a substantial amount of profit from the sale of their primary residence from federal income tax. If you meet the statutory requirements, you can exclude up to $250,000 of capital gains as a single filer, or up to $500,000 if married filing jointly. [IRS Pub. 523]

To claim this exclusion, you must pass two distinct IRS tests: the Ownership Test and the Use Test. Generally, you must have owned the property and lived in it as your primary residence for at least two years out of the five-year period immediately preceding the date of sale. [IRS Pub. 523] This “2-out-of-5-year” rule ensures the tax break benefits actual homeowners rather than short-term real estate flippers or institutional investors.

For a mid-career professional selling a $600,000 home, proper application of Section 121 means keeping the entire proceeds to fund your next down payment or retirement account, rather than losing up to 20% to federal taxes. However, calculating your eligibility becomes complex if you rented out the home, experienced a sudden job relocation, or went through a divorce. Understanding these technical nuances is critical before finalizing your real estate closing.

Structural Background

The IRS treats the Ownership Test and the Use Test as separate requirements. You must meet both, but they do not have to occur at the exact same time.

The 24-Month Rule

The required two years of ownership and use translate to exactly 24 full months or 730 days. [IRS Pub. 523] These days do not need to be consecutive. Short temporary absences, such as a two-week summer vacation or a brief hospital stay, count as periods of use. However, extended absences, such as a one-year sabbatical abroad, generally do not count toward your 730-day requirement.

Partial Exclusions for Life Events

If you are forced to sell your home before meeting the 2-year requirement, you are not entirely disqualified. The IRS grants a prorated “partial exclusion” if the sale is due to unforeseen circumstances. Qualifying events include a change in employment location (the new job must be at least 50 miles farther away), a physician-documented medical issue, divorce, or multiple births from a single pregnancy. [IRS Pub. 523]

If you or your spouse are on qualified official extended duty in the U.S. Armed Forces, the Foreign Service, or the intelligence community, you can choose to suspend the 5-year test period for up to 10 years. [IRS Pub. 523] This prevents service members from losing their tax exemption during long deployments.

Risk Layer

Taxpayers often misinterpret how periods of renting out the property interact with the Section 121 exclusion, leading to inaccurate tax filings.

The “Non-Qualified Use” Calculation

The Housing and Economic Recovery Act (HERA) introduced the concept of “non-qualified use.” If you owned the home and rented it out before moving in and making it your primary residence, that period of rental use is considered non-qualified. [IRS Pub. 523] When you eventually sell the home, you cannot exclude the portion of the capital gain allocated to that non-qualified period. The gain must be prorated mathematically based on the total years of ownership versus the years of non-qualified use. (Note: Renting the home out after it was your primary residence does not trigger this specific non-qualified use penalty, provided you still meet the 2-out-of-5-year test).

Depreciation Recapture is Unshielded

As discussed in the broader capital gains tax guidelines, if you claimed depreciation deductions while using the home as a rental or a home office, you must pay a depreciation recapture tax upon sale (capped at 25%). The Section 121 exclusion absolutely cannot be applied to shield this recaptured amount. [IRS Pub. 544]

Strategic Framework

For homeowners managing a $400,000 to $800,000 property, ensuring that your transaction fully qualifies for Section 121 requires auditing your timeline and maintaining proper documentation.

Actionable Section 121 Verification Steps

Before listing your primary residence for sale, follow this procedure to secure your tax exemption:

- Audit Your Occupancy Dates: Review your closing documents, utility bills, and moving records to verify you have physically occupied the home for at least 730 days within the last 5 years. Do not estimate; an IRS auditor will request exact dates.

- Check Previous Exclusions: Confirm that neither you nor your spouse has claimed the Section 121 exclusion on another property within the two years immediately preceding the projected closing date of this home. [IRS Pub. 523]

- Calculate Prorated Limits (If Applicable): If you must sell at 18 months due to an unforeseen job relocation, calculate your partial exclusion. (e.g., 18 months / 24 months = 75%. If married, you can exclude up to 75% of $500,000, which is $375,000).

- Determine Reporting Requirements: If your gain is fully excluded, you generally do not need to report the sale. However, if the closing agent issues you a Form 1099-S, you must report the sale on Form 8949 and Schedule D to formally claim the Section 121 exclusion and prevent an IRS automated notice. [Instructions for Form 8949]

| Taxpayer Situation | Section 121 Qualification Status | Exclusion Limit |

|---|---|---|

| Single Filer, Lived in home 3 years | Fully Qualified | Up to $250,000 |

| Married, Lived in home 12 months (Job Move) | Qualified for Partial Exclusion | Up to $250,000 (50% of $500k) |

| Single, Rented out for last 4 years | Disqualified (Fails Use Test) | $0 (Fully Taxable) |

| Married, Widowed within past 2 years | Fully Qualified (Bereavement rule) | Up to $500,000 |

If your property was strictly an investment vehicle and does not meet the primary residence requirements, you cannot use Section 121. In that scenario, you should explore a 1031 Exchange to defer the capital gains tax liability.

Frequently Asked Questions

Yes. If you receive a home as part of a divorce settlement, the IRS allows you to count the time your former spouse owned the home toward your ownership requirement. Additionally, if your former spouse is allowed to live in the home under a divorce decree, their time living there counts as your “use” time. [IRS Pub. 523]

Yes, under specific conditions. You can include the sale of vacant land adjacent to your home as part of your primary residence exclusion if you owned and used the land as part of your main home, and you sell the land within two years before or after selling the actual house. [IRS Pub. 523]

If your home is held in a standard revocable living trust (grantor trust), the IRS still considers you the owner for tax purposes. You can claim the Section 121 exclusion exactly as if the deed were held in your personal name. [IRS Pub. 523]

When you inherit a home, you receive a “step-up in basis” to the property’s fair market value on the date of the previous owner’s death. This often eliminates most of the capital gain immediately. To claim the Section 121 exclusion on any subsequent appreciation, you must personally live in the inherited home and satisfy the 2-out-of-5-year rule yourself. [IRS Pub. 551]

Series

Real Estate Tax Strategies Guide

4 of 9 articles published

Data Sources & References

- [1] Internal Revenue Service (IRS) — Publication 523: Selling Your Home

- [2] Internal Revenue Service (IRS) — Publication 544: Sales and Other Dispositions of Assets