Tax Brief: Section 221 Deduction

The IRS allows you to deduct up to $2,500 of interest paid on qualified student loans from your taxable income. Crucially, this is an “above-the-line” adjustment to income. This means you do not need to itemize your deductions to claim it; you can take the standard deduction and still reduce your tax burden, provided your Modified Adjusted Gross Income (MAGI) falls within the statutory limits.

Paying interest on student debt is generally a deadweight financial loss, but the tax code offers a specific mechanism to claw back a portion of that capital. Section 221 of the Internal Revenue Code was designed to alleviate the tax burden on graduates actively paying down their educational liabilities.

Whether you hold standard federal loans managed through Income-Driven Repayment (IDR) plans or you chose to refinance your loans with a private lender, the interest paid qualifies for this deduction. However, the IRS enforces strict income phase-out rules. You must understand how to document this expense and calculate your eligibility.

*If your MAGI falls between the two columns, your allowed deduction is proportionally reduced. IRS limits are adjusted annually for inflation.

The Four Rules of Eligibility

To legally claim this tax break on Form 1040, you must meet all four of the following IRS requirements for the tax year in question.

| The Rule | Legal Definition & Tax Impact |

|---|---|

| 1. Legal Obligation | You must be the person legally obligated to pay interest on a qualified student loan. If a parent pays a loan that is solely in the student’s name, the IRS treats it as a gift to the student, and the student claims the deduction. |

| 2. Filing Status | Your tax filing status cannot be “Married Filing Separately.” You must file Single, Head of Household, Qualifying Widow(er), or Married Filing Jointly. |

| 3. Dependency Status | No one else can claim you as a dependent on their tax return. |

| 4. MAGI Limit | Your Modified Adjusted Gross Income must be below the annual phase-out threshold (refer to the chart above). |

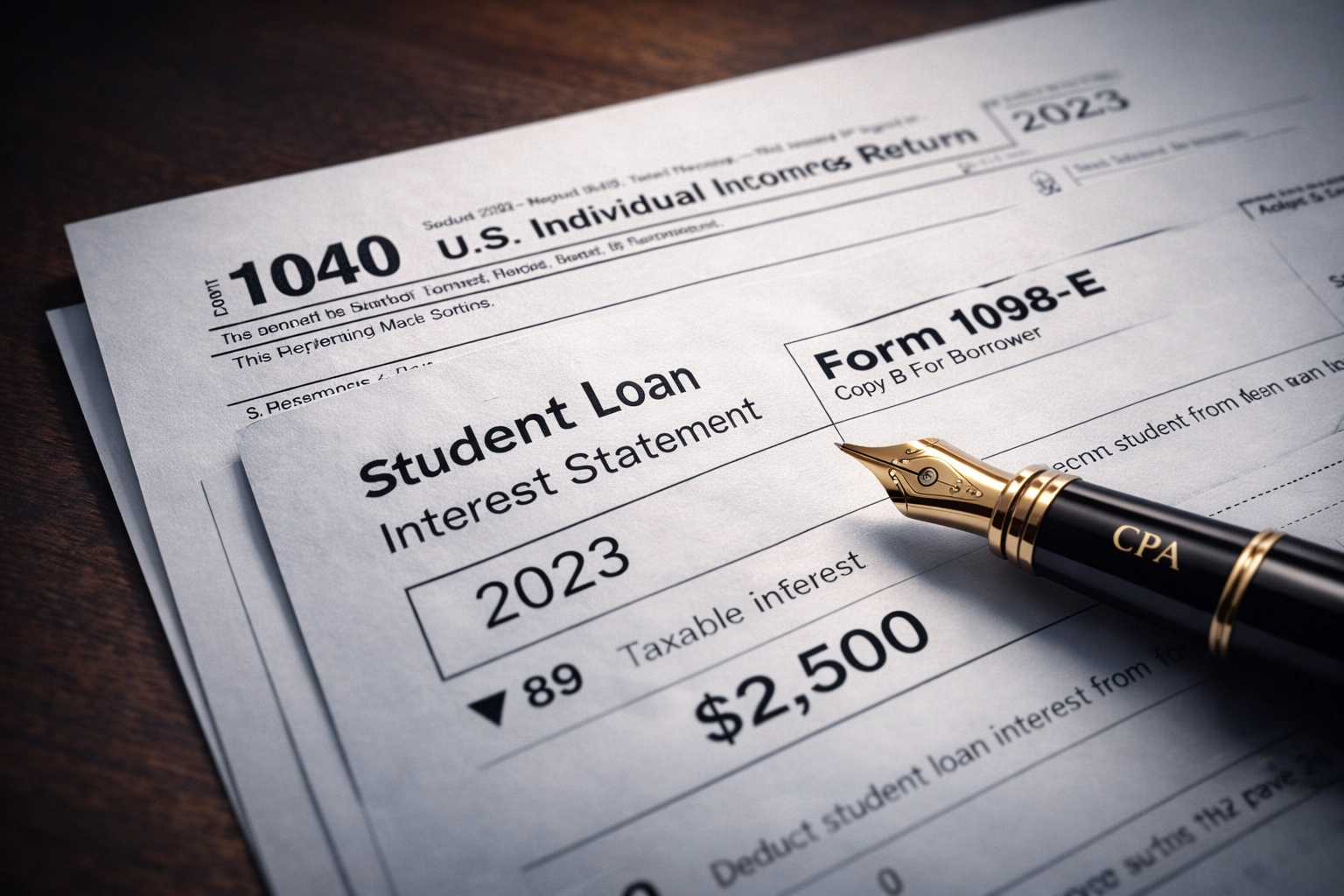

Actionable Execution: Processing Form 1098-E

Tax preparation requires evidentiary support. To execute this deduction properly, follow this documentation and filing protocol:

Your Tax Filing Checklist

- Acquire Form 1098-E: Your loan servicer is legally required to send you a Form 1098-E (Student Loan Interest Statement) if you paid $600 or more in interest during the year. If you paid less than $600, it is still deductible, but you must manually total the interest from your monthly statements.

- Combine Multiple Servicers: If you have both federal loans and refinanced private loans, you will receive multiple 1098-E forms. Add Box 1 from all forms together. Do not exceed the $2,500 maximum cap.

- Report on Schedule 1: When filing your Form 1040, enter the total allowable interest on Schedule 1, Part II (Adjustments to Income). This line item directly reduces your AGI before your standard deduction is even applied.

Frequently Asked Questions

Does capitalized interest count towards the deduction?

Yes. If unpaid interest was capitalized (added to your principal balance) after a period of deferment or forbearance, payments made on that new principal are treated by the IRS as paying down the capitalized interest first. You can deduct this amount.

What if I am pursuing PSLF and my payments are $0?

If your calculated payment under an IDR plan is $0, you are not paying any interest. Therefore, you have nothing to deduct. While you are securing the PSLF Golden Ticket, you forfeit this specific tax break, but the eventual tax-free forgiveness is far more valuable.

Can I deduct interest paid by my employer?

Under recent tax legislation (active through 2025), employers can contribute up to $5,250 annually toward an employee’s student loans tax-free. However, the IRS strictly prohibits “double-dipping.” You cannot claim the $2,500 interest deduction on money that your employer paid tax-free on your behalf.

Conclusion: Optimize Your Tax Return

The student loan interest deduction is not a loophole; it is a designed statutory benefit meant to improve your cash flow. Treating tax preparation as a passive event is a wealth-destroying habit. Gather your 1098-E forms, verify your MAGI, and ensure your CPA or tax software applies this above-the-line adjustment to lower your final tax liability.

Next Step: The Tax-Free Payment Hack

Did you know recent legislation allows you to use tax-advantaged college savings accounts to pay off your debt? Discover the rules in our next briefing: The 529 Plan Hack: Paying Off Student Loans with Tax-Free Money.