FICO vs VantageScore: Why Your Credit Karma Score Is “Fake”

You check your credit app: 720 (Excellent). You walk into the car dealership confidently. The finance manager pulls your credit and says: “Sorry, you’re a 660.” What happened? You didn’t lie; you just looked at the wrong scoreboard. Most free apps show you VantageScore (Educational), but 90% of lenders use FICO (Actual). Here is why they differ and how to find your “Real” score before applying for a loan.

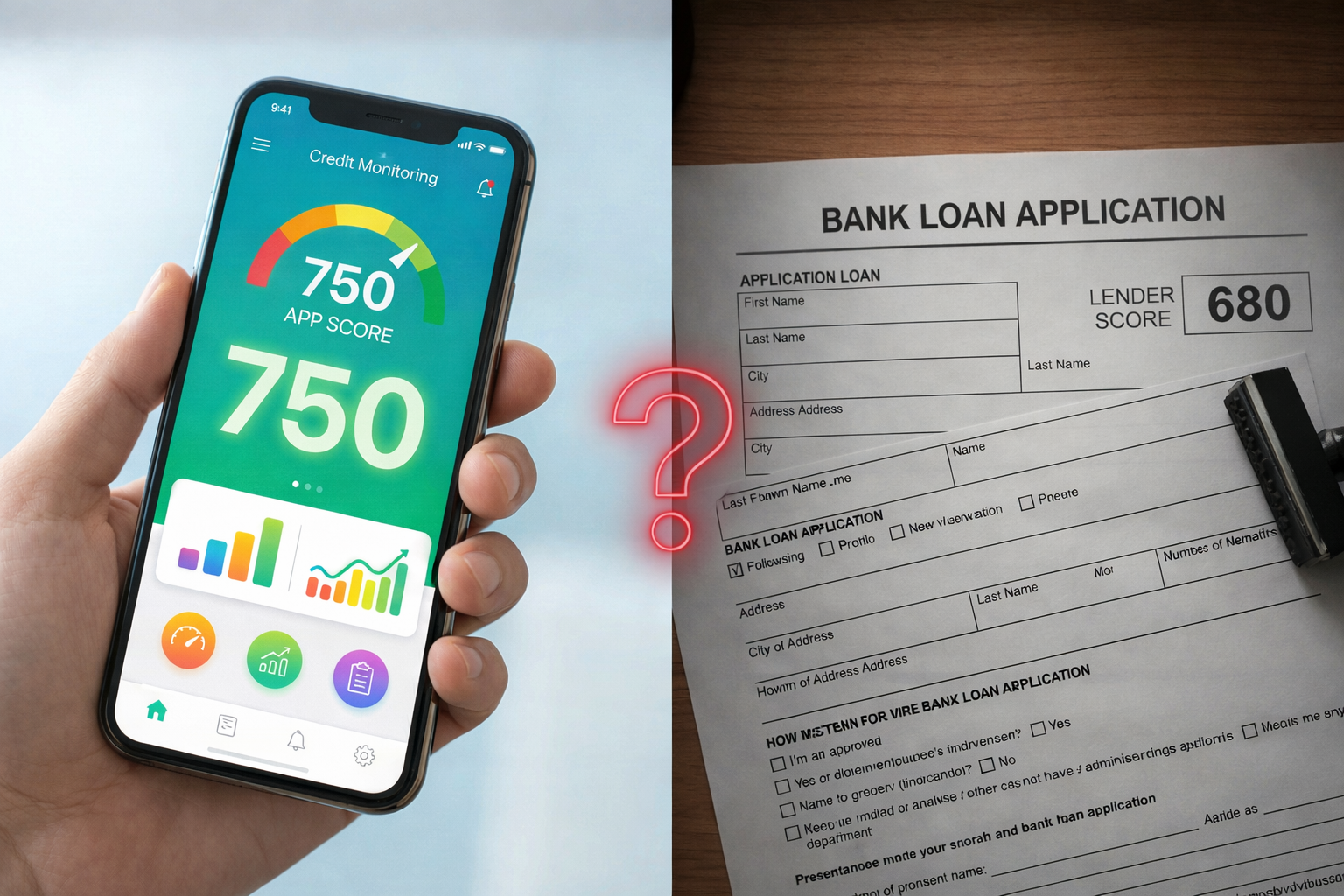

The Heartbreak Gap: Your app says you’re excellent (750), but the bank sees you as average (660). This is the difference between FICO and VantageScore.

Image Source: bestmoneytip.com

1. The Tale of Two Scores

Why do we have two different scores? Because FICO costs money to check, while VantageScore is cheaper for apps to provide to you for free.

| Feature | FICO Score (The King) | VantageScore (The Student) |

|---|---|---|

| Used By | 90% of Top Lenders | Free Credit Apps & Landlords |

| Primary Purpose | Risk Assessment (Money) | Education (Marketing) |

| Paid Collections | Counts Against You (In older FICO 8 versions) |

Ignored / Removed |

| Credit History | Need 6 months of data | Score available in 1 month |

2. Which Score Should I Watch?

It depends entirely on what you are applying for. Here is the adoption rate:

3. How to See Your Real FICO Score (For Free)

You do not need to pay $20/month to myFICO just to peek at your score. Many banks provide it as a perk.

- Credit Card Perks: American Express, Bank of America, Discover, and Citi usually show your actual FICO Score 8 on your monthly statement or app dashboard.

- Experian App (Free Version): Experian gives you their specific FICO score for free (just ignore the upsells for “CreditLock”).

- The Trap: Chase’s “Credit Journey” and Capital One’s “CreditWise” often show VantageScore 3.0, even though they are banks! Always check the fine print at the bottom of the screen.