Mortgage Interest Deduction: Why You Might Be Better Off With Standard Deduction

“Don’t worry about the high interest rate; it’s a tax write-off!” Real estate agents love to say this. As a CPA, I hate hearing it. Since the tax laws changed (TCJA), the Standard Deduction has nearly doubled. This created a massive “Hurdle” that most homeowners cannot jump over. Unless you have a massive mortgage or live in a high-tax state, itemizing your deductions might actually cost you time without saving you a dime. Here is the honest math on why your house might not be the tax shelter you thought it was.

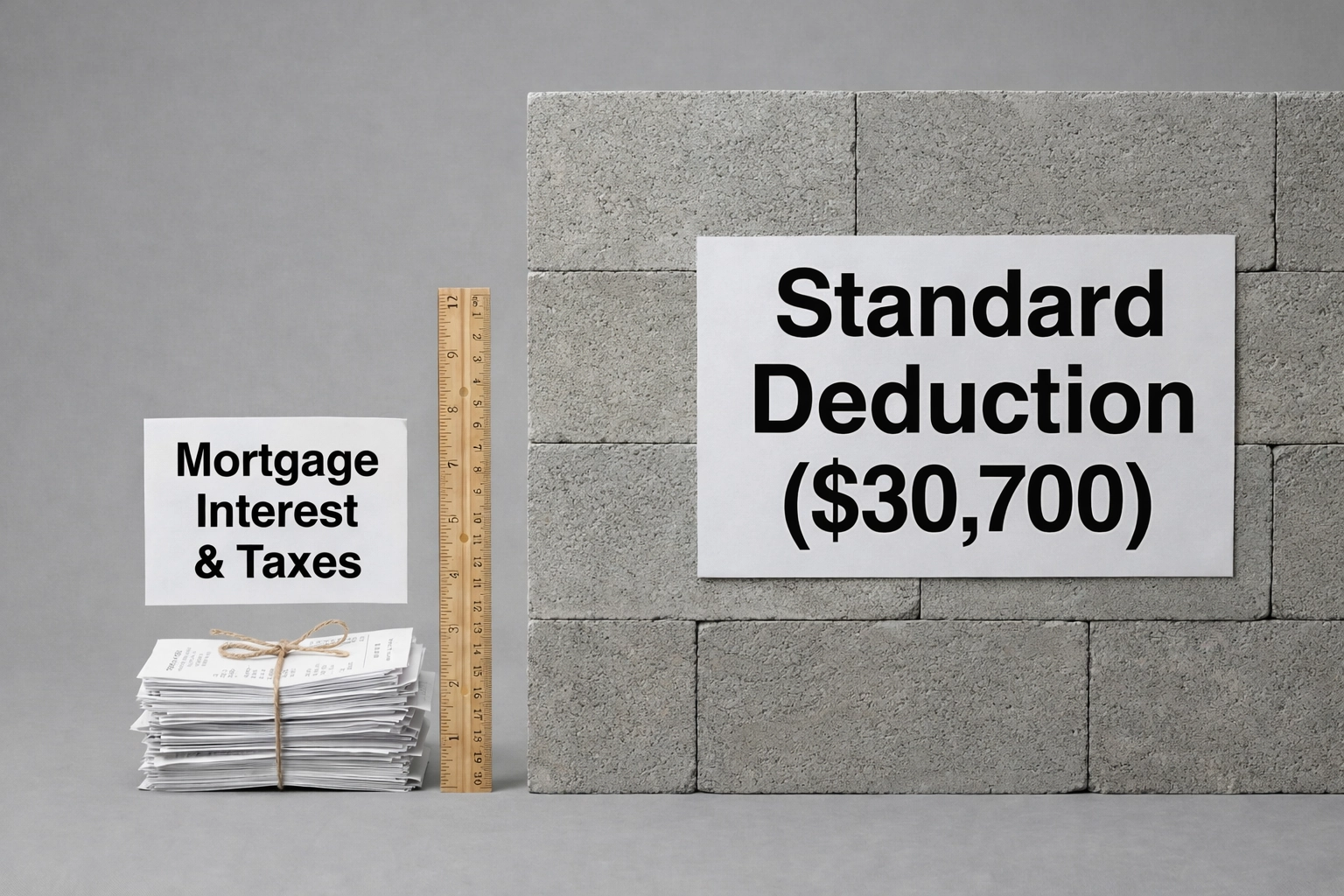

The Deduction Hurdle: Your itemized expenses (Mortgage Interest + SALT) must be taller than the Standard Deduction wall ($30,700+) to save any tax. For most, the wall is too high.

Image Source: bestmoneytip.com

1. The Hurdle: Standard vs. Itemized

You cannot take both. You must choose one:

• Single: ~$15,350 (2026 Est.)

• Married (Joint): ~$30,700 (2026 Est.)

• Effort: Zero. No receipts needed.

• Mortgage Interest

• State & Local Taxes (SALT) – Capped at $10k

• Charity Donations

• Effort: High. Must file Schedule A.

🛑 The Rule: You only Itemize (Option B) if it is BIGGER than Option A.

2. The Math: Let’s Run the Numbers

Imagine a couple buys a home for $500,000 with a $400k mortgage at 6% interest.

| Expense Category | Amount (Year 1) | Notes |

|---|---|---|

| Mortgage Interest | $24,000 | Based on 6% rate |

| Property Tax + State Tax (SALT) | $10,000 | Capped at $10k Max |

| Charitable Donations | $2,000 | Avg. household |

| Total Itemized Deduction | $36,000 | Sum of above |

| Standard Deduction (Hurdle) | -$30,700 | You get this anyway |

| Actual Tax Benefit | +$5,300 | Only the difference matters! |

In the 24% tax bracket, that saves you about $1,272 in real cash.

👉 Spending $24k to save $1k is not a good investment strategy.

3. The Double Whammy: Limits You Must Know

Even if you are rich, the IRS limits how much you can deduct.

- The $750,000 Debt Cap: You can only deduct interest on the first $750,000 of mortgage debt (for homes bought after Dec 15, 2017).

Example: If you have a $1M mortgage, the interest on the last $250k is non-deductible. - The SALT Cap ($10,000): You can deduct Property Taxes + State Income Taxes… but only up to $10,000 total.

Example: In New Jersey, you might pay $15k in property tax and $10k in income tax ($25k total). The IRS only lets you deduct $10,000. The other $15k vanishes.

4. So, Who Actually Benefits?

The Mortgage Interest Deduction isn’t dead, but it’s now a niche benefit for specific groups.

- High Mortgage: Your loan is between $500k and $750k.

- Single Filers: The hurdle is lower (~$15k), so it’s easier to beat.

- Generous Donors: You give substantial amounts (e.g., 10% tithe) to charity.