Buying Mortgage Points: Is Lowering Your Rate Worth the Cash Upfront?

“Would you like to lower your interest rate to 5.99%?” It sounds like a great offer from your loan officer. But there is a catch: You have to pay thousands of dollars at the closing table to get it. This is called “Buying Points.” It is essentially Prepaid Interest. You are betting that you will stay in the house long enough to earn that money back in small monthly savings. The bank is betting you won’t. Here is how to calculate your “Break-Even Point” to ensure you win the bet.

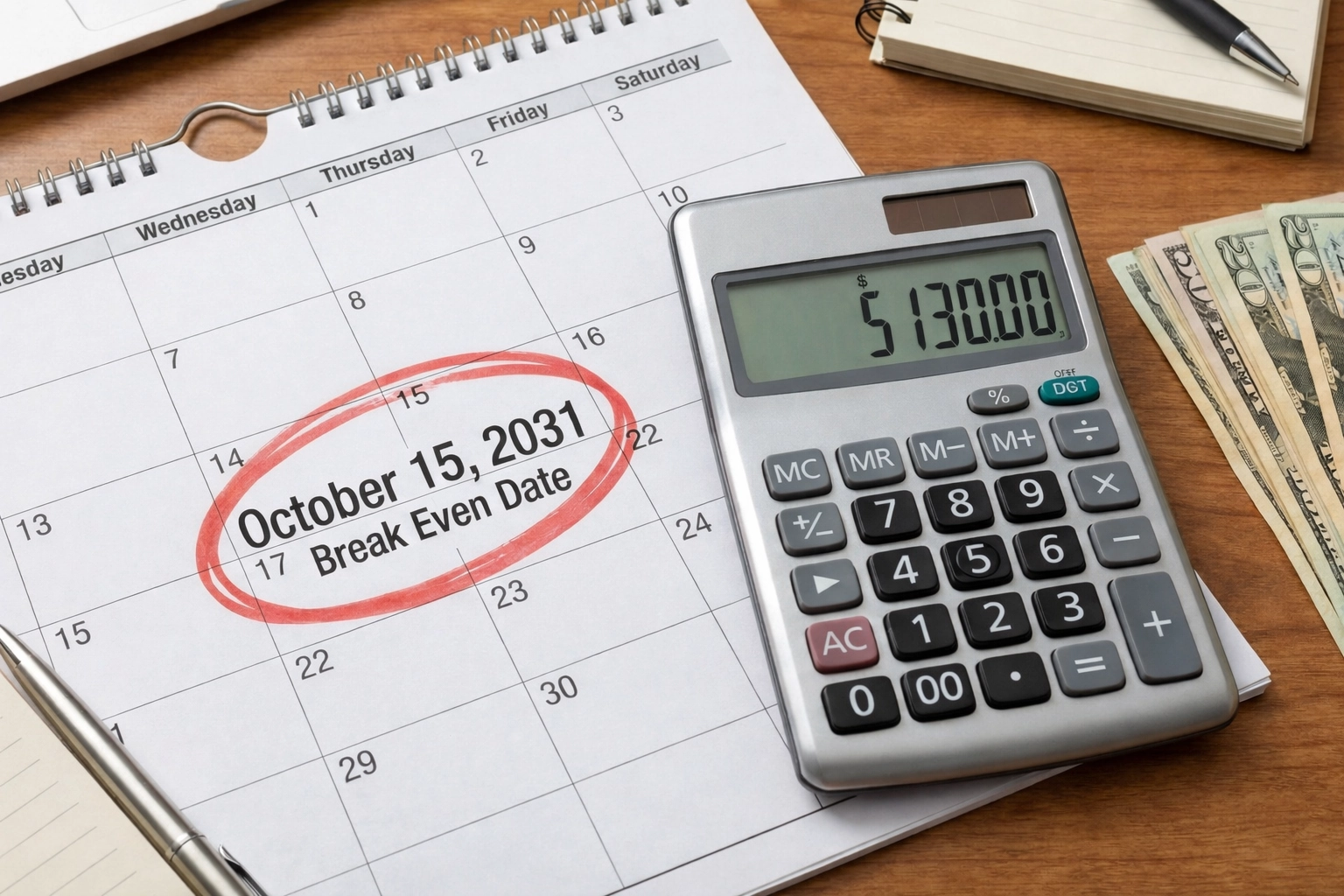

The Betting Line: Buying points is a bet on time. You must stay past the “Break-Even Date” (circled) to win against the bank.

Image Source: bestmoneytip.com

1. The Mechanics: What Are You Buying?

Think of it as a subscription service where you pay a lifetime fee upfront for a monthly discount.

- The Cost: “1 Point” costs 1% of your loan amount. On a $400,000 loan, 1 point = $4,000.

- The Benefit: Usually, 1 Point lowers your interest rate by 0.25% (e.g., from 6.5% to 6.25%).

- The Gamble: If you sell the house in 2 years, the bank keeps the profit. If you stay for 30 years, you keep the profit.

2. The Math: Do You Beat the Spread?

Let’s run the numbers on a $400,000 Loan. Is it worth paying $8,000 (2 Points) to drop the rate from 6.5% to 6.0%?

| Scenario | A. Standard (No Points) | B. Buying 2 Points |

|---|---|---|

| Interest Rate | 6.50% | 6.00% |

| Upfront Cost | $0 | $8,000 |

| Monthly Payment (P&I) | $2,528 | $2,398 |

| Monthly Savings | – | $130 / mo |

You must live in this house for 5 years and 2 months just to get your money back.

• If you move in Year 4: You LOST money.

• If you move in Year 10: You SAVED money.

3. Strategy: When to Pull the Trigger

Buying points isn’t always about math; it’s about your life plan.

- Forever Home: You are absolutely certain you will retire in this house.

- Seller Pays (Best Case): In a buyer’s market, ask the Seller to pay for a “2-1 Buydown” or permanent points instead of lowering the price. It’s free money for you.

- Rates are Low: If rates are historically low (e.g., 4%), refinancing later is unlikely, so locking in 3.5% makes sense.

- Starter Home: You plan to upgrade in 3-5 years.

- High Rate Environment: If rates are 7% today, you will likely refinance when they drop to 5%. If you refinance in 2 years, your $8,000 points fee is wasted.

- Cash Poor: Keep your cash for emergencies/repairs rather than spending it to save $100/mo.

4. The Pro Move: Use Seller’s Money

This is how smart investors use points.

Instead of asking the seller to drop the price by $10,000 (which saves you only ~$60/month), ask them to give you a $10,000 Credit towards Closing Costs.

Use that $10,000 to buy discount points. This could lower your payment by ~$150-$200/month.

Result: Same cost to the seller, but 3x more monthly savings for you.