Best Solo 401k Providers: Fidelity vs Vanguard vs E*TRADE

Opening a Solo 401k is not like opening a checking account. The features depend entirely on the “Plan Document” provided by the broker. Most investors flock to Fidelity because it is free, only to discover later that it does NOT support Roth contributions or Loans. Surprisingly, E*TRADE has emerged as the feature king among free brokers, offering both Roth and Loan options that others charge for. If you want a wealth-building Ferrari without the fees, you need to choose carefully. Here is the definitive comparison for 2026.

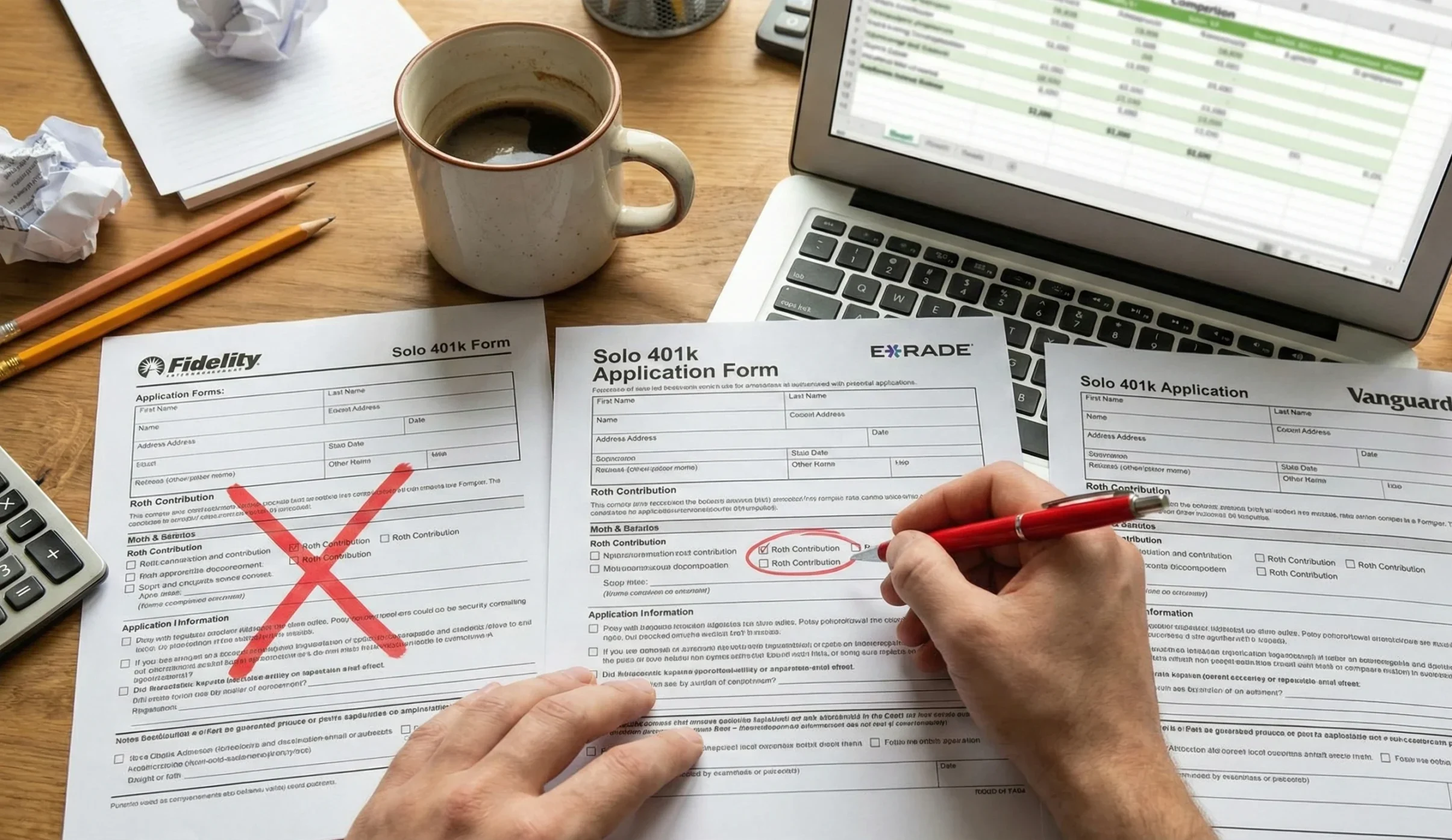

The forms tell the story: E*TRADE explicitly offers the Roth option that others miss.

1. The “Free” Trap: What Are You Missing?

“Free” usually means “stripped-down.” But one broker is breaking the mold.

- Cost: $0 Setup

- Roth: ❌ NO (Pre-Tax Only)

- Loans: ❌ NO

- Cost: $0 Setup

- Roth: ✅ YES (Fully Supported)

- Loans: ✅ YES (Rare for Free Plans)

2. Fidelity vs Vanguard vs E*TRADE (Checklist)

Here is the side-by-side truth. E*TRADE is the surprising winner for features.

| Feature | Fidelity | E*TRADE | Vanguard |

|---|---|---|---|

| Setup Fee | $0 | $0 | $20/fund (waived usually) |

| Roth Option | NO (Standard Plan) | YES | YES (Roth 401k) |

| 401k Loans? | NO | YES (Up to $50k) | NO |

| Verdict | Good for Pre-Tax only | Best Overall | Fees increased |

*Note: Vanguard recently sold its Solo 401k business administration to Ascensus, adding fees and complexity. We currently recommend E*TRADE for new accounts due to the loan feature.

3. Strategy: When to Pay for a Plan

Even E*TRADE has limits.

- Scenario A: You want to buy Real Estate. Standard brokers (even E*TRADE) only let you buy stocks and bonds. If you want to use your 401k to buy a rental property, you MUST pay for a Custom Plan Provider (e.g., MySolo401k, Nabers).

- Scenario B: Mega Backdoor Roth. While some brokers allow basic Roth, the massive “Mega Backdoor” strategy (contributing up to $69k+ in after-tax dollars) usually requires a custom plan document.

- How it works: You pay the provider ~$500 for the legal documents. You then take those documents to a bank to open the account.

4. Warning: The Administrator Burden

With great power comes great paperwork.